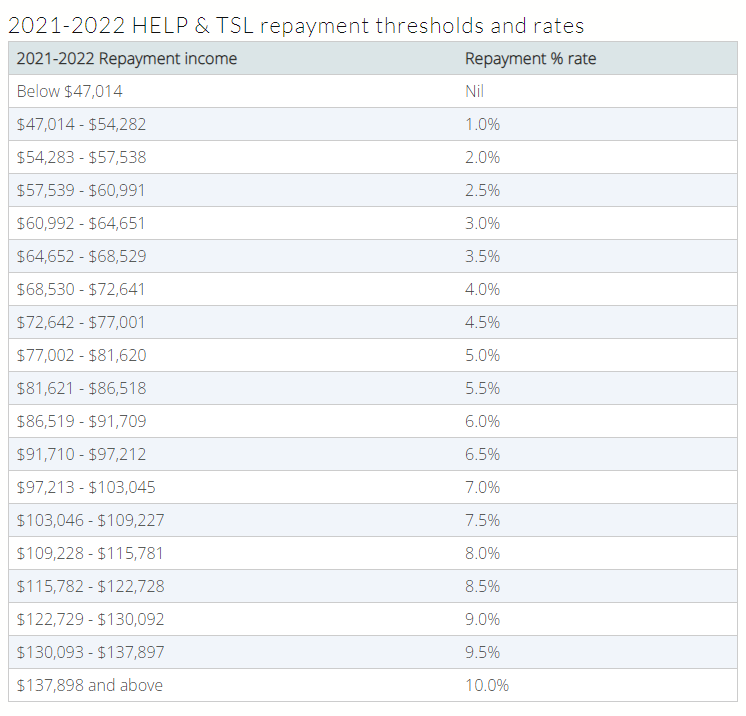

The High Education Contribution Scheme (HECS) or Higher Education Loan Program (HELP) is effectively a Government loan that enables people to afford the costs of higher education. The program works by allowing people to pay back their student loans at a time in the future when they are earning enough money to comfortably cover the payments. In the last decade, the cost of higher education has skyrocketed, and this has forced many students to take up a program like HECS or HELP, so they can continue their education. Once they have completed their education, most people never really think about the impact of HECS debts, as it is normally something that is taken care of at tax time. The repayment rates are generally quite low and not overly burdensome for most people. However, what many people don’t realise is that these student debts will have an impact on your ability to borrow money when the time comes to buy a house. This can be particularly impactful for people like first home buyers, or even those on high incomes, as the repayment rates increase sharply. When banks and lenders assess your ability to service debt, what they are doing is determining your normal income and expenses, with the understanding that you will be able to service debt with spare income. If you are carrying a large amount of student debt that you are required to pay back by law, it can weigh heavily on your ability to borrow. For a lot of people, a few hundred dollars per week can be the difference between buying a home and not being able to get finance. For that reason, it is very important to understand what your student debt looks like and the level of repayments that you’re required to be making. This is the current repayment table.  If your income falls below $47,014, you’re not required to pay back any of your HECS debt. This is the category into which people who are new to the workforce will most likely fall.

By the time you are earning around $100,000 per year, you will be required to pay back approximately 7.5% of the total outstanding student debt. For a HECS debt of around $50,000, that could see your borrowing capacity reduced by anywhere from $75,000 - $100,000, which is quite significant if you’re looking at buying your first home. The reality is that the majority of Australians will have some form of student debt that they are required to pay back. The best option is to always speak to your mortgage broker and get a clear picture of your borrowing capacity well before you even look to put in an offer on a property. That way, regardless of your situation and current income and expenses, you will know where you stand. See your home loan options in less than 5 minutes |

EDITOr

Categories

All

Archives

December 2023

|

RSS Feed

RSS Feed

|

|

Read about us on KochiesBusinessBuilders and Linkedin

Partner with Adobi Mortgage Solutions Contact Bruce Johnstone (03) 9996 8553 or email [email protected]

|

©2021 ADOBI® MORTGAGE SOLUTIONS ABN 94465268443

Suite 405, 585 Little Collins Street, Melbourne, VIC 3000 Telephone: (03) 9996 8551 Credit Representative Number 536529 authorised under Australian Credit Licence 384324 Your complete financial situation will need to be assessed before acceptance of any proposal or product Please review our Lenders, Terms of Use and Privacy Policy Member 87449: AFCA - Australian Financial Complaints Authority Member M-351557: FBAA - Finance Brokers Association of Australia |