|

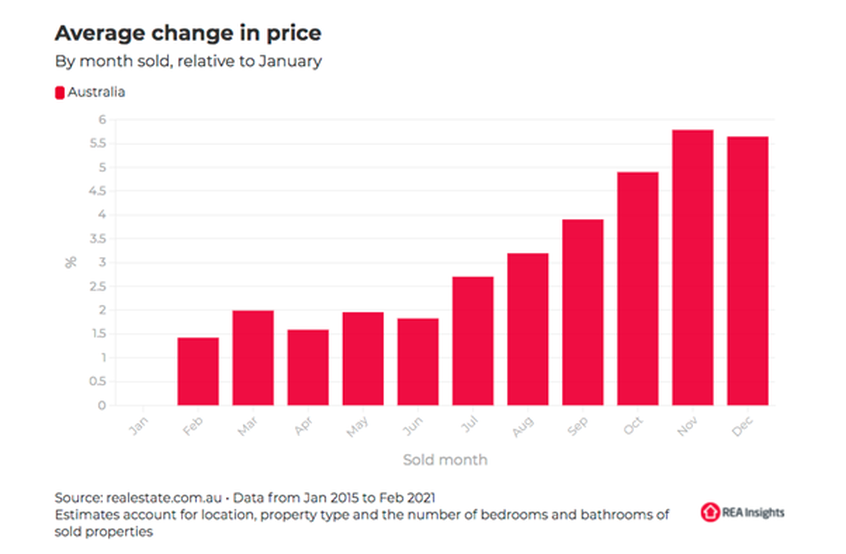

With the spring selling season coming to an end and Christmas just around the corner, many buyers and sellers are getting ready for a well-deserved break. The traditional belief is that spring is the best time to sell and it’s for that reason we see the largest volume of transactions taking place throughout September, October and November. This is followed by a sharp drop in transactions over the summer months. Interestingly, if you’re a buyer, then summer could well be an opportunity for you to find a great property at a decent price. In fact, research from realestate.com.au suggests that if you’re a buyer, January might be the month that represents the best buying opportunities.  Source: realestate.com.au

This data found that across the country, properties sold in November have attracted prices almost 6% higher than those in January. According to the numbers, January has been the cheapest month to buy a property over the past three years. However, there are some big differences in the various capital cities, with the biggest seasonal impact being felt in Sydney, Melbourne and Hobart. Across these three capital cities, houses sold for prices in December that were 10% higher than in January. The belief is that in spring there are more auctions taking place, which leads to higher prices in Sydney and Melbourne in particular, which feature the majority of auctions. The fact that January can attract lower prices also has to do with the fact that many properties that might not have sold in December were held over until January. The impact of the time you buy and sell is a lot less prominent in other capital cities, but it still does occur in both Brisbane and Adelaide. In Perth, it appears that the best time to buy is during the winter months. As we move into the new year, the question remains, will this trend continue? 2021 hasn’t been a normal year by any standard, however, transaction volumes are getting higher each week as many people who have been holding off on buying or selling finally start to get active. See your home loan options in less than 5 minutes  Traditionally, the Christmas and New Year period is the time of year where many of us tend to overspend. While this might be well-meaning, as most people are simply buying gifts for family and friends at Christmas or going on holiday, you need to be sure that it doesn’t blow your budget.

If your goal is to buy a property in the new year, then it’s important to not let a Christmas splurge get in the way of your real estate dreams. Here are a few ways to better manage your money ahead of the holiday season. Put the Credit Card Away The problem with credit cards is they are easy to use and not always easy to keep track of. During the lead-up to Christmas, it’s very easy to get carried away spending. This can not only hurt your savings, but it also makes it appear that your typical spending habits are a lot higher than they might be. A lender will take close look at your expenses over the previous three months when assessing a home loan application, and if they are excessive, it could dent your serviceability and risk getting your loan application rejected. If you don’t particularly use or need your credit card, it can often be a good idea to get rid of it altogether, as lenders assess your credit card as if it is fully maxed out. Allocate Funds in Advance We all know that budgeting is important but for most people it is not only hard to do, but hard to implement. One of the best ways to effectively budget is to allocate all your spending money in advance and put it on a debit card. This way, there is no chance you can go over budget. It’s even possible to have multiple debit cards for different areas of your life, such as essentials, spending money and things like bills and expenses. Then, you simply transfer funds to them each week. While this might seem a little over the top, if your goal is to get on the property ladder, then it might be well worth going to these lengths for even a short period of time. Avoid Borrowing While it might be very tempting to jump on a plane after what has been a few rough years for those that love to travel, don’t take on any debts in the process. Many people like to put their holidays on credit or even take out a personal loan. The problem with adding debt is that this money needs to be paid back. When you have debts, it weighs on your serviceability. Given that credit cards and other unsecured debts attract incredibly high interest rates and need to be paid back in a matter of years at the latest, this can really hurt your bottom line when applying for a loan. For first home buyers, even a $100 per week payment on a credit card or loan could be enough for you to miss out on getting a loan for your first property. If your goal is to buy a property, wait until you’ve settled on the property and made a new budget before going out and spending money you don’t have on a trip. See your home loan options in less than 5 minutes  With the holiday season fast approaching, millions of Australians are more excited than ever to get away. One of the most popular holiday options in recent years has been heading off in a caravan or camper for a road trip. Before going out and buying a caravan or camper, it’s well worth thinking about how you’re going to finance it. Given that a caravan or camper are normally the second largest purchase most people will ever make – after the family home – it’s wise to have things organised well in advance.

Typically, those looking to purchase a caravan or camper have a range of different options. While some people will pay cash, the vast majority will look to finance the purchase with some form of loan. The types of loans that are on offer can be similar to car loans, with the most attractive options normally loans that are secured by the caravan or camper itself. However, there are a number of choices including unsecured loans and personal loans. For people that are unfamiliar with the finance process, they might go directly to the dealer and look to obtain finance that way. However, there can be several limitations if you’re only speaking to a dealer for your finance. Dealer vs Broker While the finance process might be quick if you speak to a dealer, it could end up costing you more in the long run. Dealer’s will likely not be looking to get the best deal for you and will often only work with a specific lender. If you talk to a broker beforehand, they will be able to assist you in finding the best deal suited to your needs, as they have access to a panel of lenders. At the same time, a broker will also be able to look at your personal situation and explore the best finance options that include other considerations, like your mortgage. If you have a home loan already in place, then it could be possible to redraw or even refinance in a bid to use some of the equity. It might even be possible to obtain a lower rate if you’re using your home loan. There are also other levels of flexibility that you can explore with the financing of your caravan or camper, such as having a balloon payment. A balloon payment allows you to have lower ongoing payments and then make a large one-off payment at the end of your loan. However, this might end up costing you more in interest. The other advantage of looking to obtain finance through a broker is that you can organise a preapproval well in advance. That gives you the peace of mind that when you go out and start looking, what you’re buying is well within your budget. Obtaining finance for your new caravan or camper doesn’t have to be difficult, but it’s worth speaking to a broker to assess your options well in advance. See your home loan options in less than 5 minutes See your vehicle finance options in less than 5 minutes |

EDITOr

Categories

All

Archives

December 2023

|

RSS Feed

RSS Feed

|

|

Read about us on KochiesBusinessBuilders and Linkedin

Partner with Adobi Mortgage Solutions Contact Bruce Johnstone (03) 9996 8553 or email bruce@adobi.com.au

|

©2021 ADOBI® MORTGAGE SOLUTIONS ABN 94465268443

Suite 405, 585 Little Collins Street, Melbourne, VIC 3000 Telephone: (03) 9996 8551 Credit Representative Number 536529 authorised under Australian Credit Licence 384324 Your complete financial situation will need to be assessed before acceptance of any proposal or product Please review our Lenders, Terms of Use and Privacy Policy Member 87449: AFCA - Australian Financial Complaints Authority Member M-351557: FBAA - Finance Brokers Association of Australia |